Hookipa (OTC:HOOK)

or: the art of investing with minimal effort

When you buy or sell a stock you should always worry that your counterparty has done better research, has faster access to new information, or, generally speaking, that the market is right. It often is, in my experience. You think you know an obscure OTC-listed seller of screwdrivers pretty well but it turns out a Twitter account with ten followers has weekly calls with the CEO and models the company backlog on a day-to-day basis in a 100-page spreadsheet. Always manage your portfolio with that in the back of your mind1.

But every now and then you encounter a situation where there is just not much to research. Only a snippet of information is available and you have to roll the dice based on that snippet and the stock price. I have a soft spot for situations like that - I am lazy and if there is nothing to do it reduces the chance that somebody will get the better of me through sheer hard work.

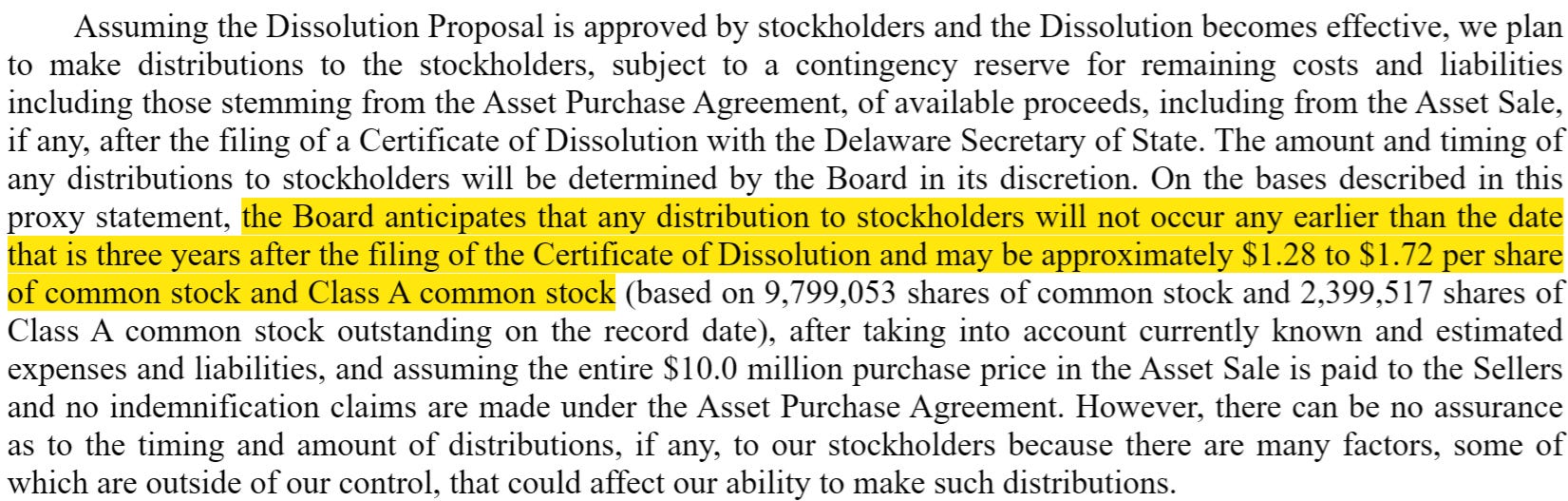

Hookipa Pharma (OTC:HOOK)2 is a nice example. It is a busted biotech that, after backing down from a stupid merger, decided to throw in the towel, sell its assets and liquidate. I own some shares and my whole thesis is based on a single line on page 43 of the latest proxy statement:

There are no detailed financial projections in the proxy statement. There is no pro forma balance sheet. There are no recent financials. I don’t expect future financials. You can try to make an extensive model in Excel based on the limited information that is out there but if push comes to shove would you rather trust that than what management is saying?

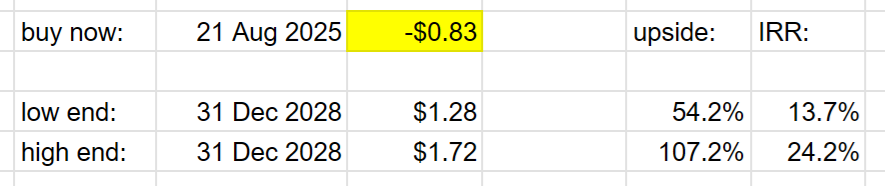

The vote to liquidate has already passed. Shares traded at $1.15 before the company announced on July 18 it would delist from the NASDAQ. Since then shares dropped over 25% on no news whatsoever from either Hookipa or Gilead (the asset purchaser).

I think this checks a lot of boxes for potential mispricing. It is an illiquid3 nanocap, recently delisted, buying implies a brutal 3-year lockup of capital, it’s a black box and on top of all that it doesn’t even do crypto treasury. But I’ll gladly take all that for an uncorrelated 15% - 20% IRR.

Now as I said previously, I am lazy. But I didn’t just buy a ton of shares directly after seeing that one sentence in the proxy (it was pretty close though!). I’m not going to spoon feed you everything that I did, but here is some of the stuff that I would recommend doing before you hit the “buy” button:

Make sure that the latest quarterly financials in combination with the Asset Purchase Agreement and your assumptions about the liquidation square with the expected payout.

Understand the capital structure and make sure that it is appropriately reflected in the share count given in the snippet I pasted above.

Assess the risk of Gilead disputing the transfer plan payments and the effect that has on the estimated payouts.

Look at the shareholder base, the board and the management suite. Are there any notorious fraudsters or scumbags involved? Any activists? Do insiders own stock?

Read the background section of the proxy to see if anything stands out (for example: were there alternative suitors?).

Ensure there are no legal issues outstanding4.

Check whether you agree with my timeline.

If you find anything interesting, please let me know. Maybe I am wrong and there is more due diligence to do! Also, should I continue using footnotes as much as Matt Levine or do you hate that format?

Finally,

The legendary Alpha Vulture wrote a good blog post about this.

Maybe it’s just me but isn’t that a terrible company name? “HOOKIPA Pharma” conjures up an image of doctors chilling in a shisha bar. The enormous cash burn since the company started exploring strategic alternatives over a year ago suggests it is a high-end shisha bar.

As an aside I love to dabble in illiquid stocks. However, sharing illiquid ideas is not always a smart idea. Yes, I might get some good feedback but if only a few readers decide to put in orders I’ve effectively shut down my own opportunity to buy or sell more at attractive prices. Hookipa is basically at the bottom of the range of stuff that I am willing to share. Always be skeptical about people hyping illiquid stocks - often they’re literally trying to sell to you.

Even a single lawsuit can completely derail a nanocap liquidation. Always check out the ‘Legal Proceedings’ section in the 10-Q. I also recommend to use CourtListener to search for potential lawsuits.

Interesting to see they sold oncology assets, but assume they’re not worth much considering no price was disclosed. On the other hand, the timeline is extending out already, considering they haven’t filed for dissolution yet and the proxy notes any distributions would be at least three years after filing. Thanks for this write up by the way, I bought some after reading.

What a fascinating little read that turned into a much longer read! Thx for sharing. I wish I saw this a little sooner. I saw something in the proxy about locking down the list of registered shareholders on what they call the 'Final Record Date'. This is a little unsettling if one were to pursue something through an OTC transaction. There is risky and then there is silly. Curious...I am still seeing active trading on HOOK with reasonable volumes, all things considered. Am I missing something?