Downside Protection? (AIRI)

Defense industry special situation.

Air Industries Group (NYSE:AIRI) is a small subcontractor operating in the US defense industry, making complicated stuff like landing gear for the F-18 and flight controls for Black Hawk helicopters. The company has been around for decades and has a solid revenue track record. Unfortunately, Air Industries is subscale, overleveraged, and as a result structurally unprofitable. Making cool gadgets does not equal making money …

Last week, the company announced a strategic combination with Tenax Aerospace, an unlisted defense company. It looks like a typical reverse merger: a stock/stock deal, AIRI shareholders will own only ~5% of the combined company, limited disclosure so far. Understandably, the market reaction was lukewarm and AIRI traded down on the announcement.

However, there is some fascinating stuff in the small print. Most notably1:

If the average volume weighted price of Air’s common stock during the twenty trading days prior to the closing is less than the Debt Adjusted AIR Share Price, the Merger Agreement calls for Air to commence a tender offer to acquire up to one million shares of Air’s current shareholders’ common stock. In addition, on the first anniversary of the merger, shareholders of Air as of the business day immediately prior to the closing of the merger will have a contingent right, subject to specified conditions, to require Air to redeem their remaining shares if the twenty-day volume weighted average price for Air shares preceding such anniversary is less than 107.3% of the Debt Adjusted AIR Share Price. This redemption right will not be transferable.

What is the Debt Adjusted AIR Share Price? As per the press release, based on preliminary December 2025 balance sheet, $3.44. And according to the merger agreement:

WHEREAS, as of or prior to the Closing, AIR and a rights agent mutually agreeable to AIR and Tenax (the “Rights Agent”) will enter into the Redemption Rights Agreement, pursuant to which the AIR Stockholders as of the Business Day prior to the Closing will have the right to cause AIR to redeem their shares of AIR Common Stock for an amount in cash equal to 107.3% of the Debt Adjusted AIR Share Price (such amount, the “Redemption Price”) following the first anniversary of the Closing Date;

So, based on the preliminary balance sheet we have the right to sell our shares at $3.69 in about 15 months2. That sounds interesting! Let’s dig in a bit.

Valuing the redemption right

To start with, let’s look at that $3.44. Where does it come from? As per the merger agreement, AIRI is valued at $20.5m minus (plus) any net debt over (under) $24.6m at the time the deal closes - the ‘AIR Debt Target Amount’, divided by the target number of shares: 5.26m. Net debt is calculated as indebtedness plus most other liabilities on the balance sheet minus cash and merger expenses. If net debt is exactly $24.6m the adjusted share price would be $20.5m / 5.26 or $3.90. So as of December, net debt is a bit higher than the debt target.

Should we expect more cash burn until the merger closes? Is the $24.6m debt target in the merger agreement unrealistic? Possibly. But cash burn the past few years has actually been minimal on average. On top of that, the latest 10-Q mentions:

As a result of recent contract awards, as of September 30, 2025, the Company had total unfilled contract values amounting to $269.0 million (including its $131.8 million in backlog plus additional potential funded orders against Long-Term Agreements (“LTAs”) previously awarded to us). These unfilled contract values support a positive outlook for future growth; however, extended lead times for raw material procurement and the complexity of manufacturing processes are expected to delay revenue acceleration until early 2026.

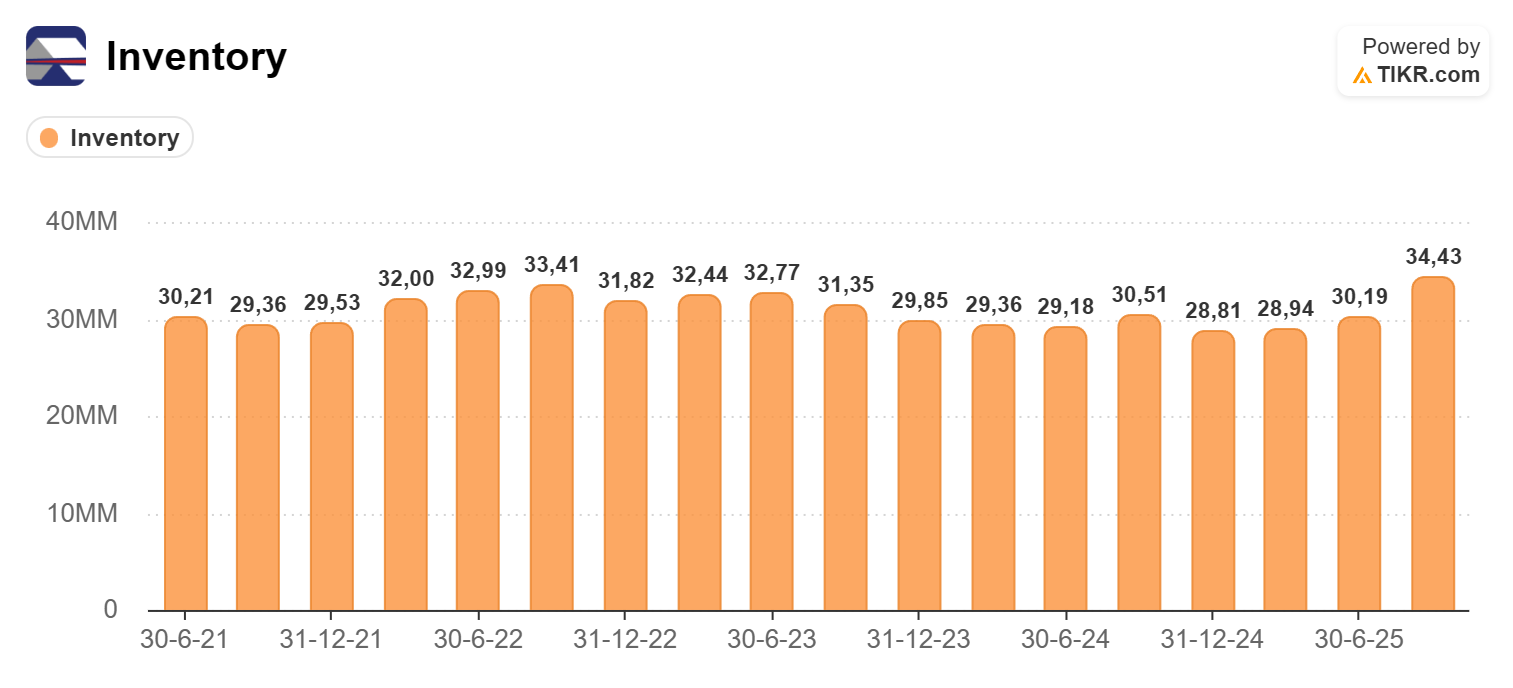

It appears to me that inventory levels are slightly elevated as well (see graph below). Perhaps the company expects to free up some working capital during the next few months. Note that most current liabilities are part of the net debt calculation but receivables and inventory are not, so there is room for some creativity here. Insiders own close to a million shares and are, as such, somewhat incentivized to free up working capital.

And finally: as per the press release AIRI shareholders are expected to own 5% of the combined company. We can deduce the Debt Adjusted AIR Share Price from that. If the debt adjusted share price is small there will be more dilution and vice versa. A 4.5% ownership implies an adjusted share price of $3.313 and 5.5% ownership implies an adjusted share price of $4.05. Seems to me that the company is expecting minimal cash burn or even a small release of working capital the next few months.

What is the present value of a stock with a built-in redemption right? We could do some complicated math but I propose to keep it simple: let’s focus on the downside. I am working with the assumption that the company is not going to burn any cash in the next few months. As outlined above, I think that assumption is reasonable, perhaps even conservative. That means that in 15 months you’ll be able to sell your shares at $3.69. I’m going to discount that back at 15% p.a. to account for counterparty risk4 for a $3.10 present value of the redemption right. On top of that you own a call option on the stock being worth more somewhere in the next 15 months. That call is also worth a few cents to a few dimes, depending on your assumptions.

Closing thoughts

There’s a lot of stuff I didn’t touch in this write-up. Insider ownership and related party loans, the history and leadership of Tenax and AIRI, termination fees, the potential tender offer at closing, what happens if the deal breaks, etc. As always, I am lazy, I don’t want to hold your hand. You should do your own due diligence and if you disagree with me or think I made a mistake I’m all ears.

That said, I think this actually looks like a sensible deal. At the very least the two companies merging build and sell tangible widgets and operate in the same industry. That is already a big step up from the average reverse merger5.

AIRI insiders avoid bankruptcy, get back the money they loaned to the company and retain the upside of their ~17% stake in AIRI with a cash floor.

And on the other side of the deal, for ~5% dilution Tenax buys a public listing and a tuck-in acquisition with a $269m order book where they can probably cut some costs. The current AIRI stock price implies a ~10x EV/EBITDA multiple. That is certainly not cheap but not crazy either. With a protected downside, a low float and an industry with some tailwinds, who knows what can happen.

Just after the deal was announced AIRI traded below $3 and I think that was a very decent proposition. Unfortunately shares traded up a bit since and the current price looks slightly less attractive to me now. I still own a decent chunk. If AIRI manages not to burn too much cash during the next few months you are paying very little for a call option on the Tenax listing. If the company actually frees up some working capital you get the call option for free.

As always, I encourage you to do your own work. My advice in situations like this is to not focus on a single number (i.e. the $3.44 from the press release) but on a range of outcomes. What happens if the company unexpectedly burns through $3m the next few months? How does changing the discount rate to 20% affect the present value of the redemption right? What happens in case of a deal break? How likely is a deal break? Make your assumptions explicit and play around with them. That way you get a feeling for what is important and what is not and you can quickly adapt when circumstances change.

There’s also a potential tender offer!

The deal is expected to close in Q2 2026.

$387.04m / (5.256 / 4.5%) equals $3.31, see the bottom of page 24 of the merger agreement.

This is not a centrally cleared put but a subordinated obligation from Tenax.

Where a busted biotech merges with a startup trying to mine lithium in space valued at $500m, or something similar.